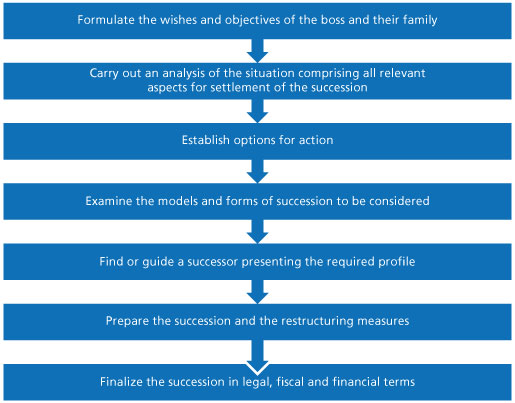

Think about your company succession sufficiently in advance

Since a successful company transfer usually takes several years, an entrepreneur has everything to gain by reflecting on their succession as early as possible, in order to correctly plan the stages and avoid any unpleasant surprises.

It is wise to think about succession once you enter your 50s. It is considered early if it occurs at the age of 60, normal between the ages of 62 and 65, and late after the age of 68.

In all cases, prudence and considerable thought are required on the part of the entrepreneur facing the challenge of their own succession. They are recommended to carefully consider all succession options and prepare to change strategy during the process if necessary (for example, if a natural heir withdraws during the transfer process).

Good communication is key

Once the transfer process has been triggered, this information needs to be communicated to all interested parties, including within the company. Effective and transparent communication plays a crucial role in the success of the operation and its acceptance by employees. It also makes it possible to counter false rumors spread by managerial staff, employees and customers, anxious about the future of the company. It is important for information about the succession process to be communicated in-house first of all and then to the public. Otherwise, the effect could be disastrous for employees who could feel betrayed by their company. There is nothing worse for a business in the process of being taken over than to lose the confidence of its managerial staff and employees who then leave the ship.

Of course, these principles of clarity and transparency do not exempt the interested parties from the necessary discretion regarding the financial or other details of the operation, which may form the subject of a written confidentiality declaration.

Optimizing the value of the company

Succession planning also includes financial and management aspects. It will be even easier for a company to find a buyer if its finances are healthy, its organization exemplary and its accounts irreproachable. It is also the duty of a responsible entrepreneur to make sure that they are handing over their company in such a way that their successor is able to take control in the best possible circumstances. In any case, when preparing their succession, they must review the organization and management of the company and improve its functioning where applicable, particularly when the company has been managed rather informally. A company looking for a buyer must also have transparent accounts and effective indicators of its good health. These provisions play a key role when it comes to negotiating the value of the company.

Taking tax aspects into account

Succession obviously involves various fiscal aspects. This issue should be tackled well before the succession actually takes effect. In the presence of statutory heirs (spouse, children, etc.), these issues absolutely must be discussed within the family so as to reach compromises that suit all interested parties.

Entrepreneurs are recommended to verify, as a minimum, the following elements:

- Loan to finance the takeover. If the takeover of the company is funded with borrowing, the interest payable and its repayment (over time) by the successor (borrower) are taxable in full. Does the company acquired generate enough income to allow the successor to repay debt, pay taxes and make a living, without being required to remove too much of the company’s cash, thus blocking any investment?

- Double taxation. In the context of capital companies, the company’s profit is liable to double taxation: firstly on the company’s profit and secondly on the business owner’s income. A consequence of this double taxation is the tendency to not distribute the profits made and to invest them in the company. This “weighs down” the company. It often happens that profits invested in this way cannot be recovered in the sale price for the company, because they are only rarely components of the value of return.

- Indirect partial liquidation / heirs’ holding company / transposition. If entrepreneurs set up a company financed by third parties with a view to taking over a company, they need to act with extreme caution. They are strongly recommended to use a tax expert.

- Succession / gift duties (cantonal laws). Transfer to indirect descendants can have significant fiscal consequences (up to 40% of the value of the company). Since tax has to be paid within very short timeframes, the resulting cash and financing requirement is significant.

- Financial restructuring. The transfer of elements of the company’s assets to private assets, and vice versa, can have fiscal consequences if carried out within five years before the day of reference for the official transfer of the company. Entrepreneurs are recommended to plan such measures well in advance.

- Buyout company. If the successor or heir would like to set up a buyout company to take over the operating company, consulting a tax expert is essential.

Ensuring your future after succession

Life continues for the entrepreneur after the completion of the transfer of their company. Retirement requires considerable thought on the part of the entrepreneur about how their future will be assured. Often, the income paid via OSI, annuities from the pension fund or old-age insurance is not enough for the entrepreneur to continue with their former lifestyle. Some financial assets which are not essential to the company can thus be contributed to the seller’s private wealth. They are recommended to use the services of an experienced financial advisor who will be able to offer advantageous individual investment or fiscal optimization solutions.